Retirement Savings

I have found that professional, super-smart people, that I personally know, do not know the difference between an IRA, a Roth IRA, and a 401(k). That will simply not do. You need to know this stuff. We’re going to fix that right now. The challenge will be keeping it short and sweet because there are sooooo many things I want to say.

In part 1, we will discuss the differences between IRAs and 401(k)s. Then in part 2, we will talk about the differences in the Roth versions of these same things.

To help illustrate this, we’re going to think of these things as buckets. A bucket holds things. In this instance, the bucket is going to hold money. You want to put your retirement money in one of these buckets. Which one? Well, that depends.

IRA — IRA stands for Individual Retirement Account.

Quick History: The IRA was established when Congress passed the ERISA (Employee Retirement Income Security Act) in 1974. People LOVED this idea, so another act was passed (the Economic Recovery Tax Act of 1981 or ERTA) to make the IRA available for all workers under 70 ½, and to increase the contribution limit. Different laws increased allowable IRA contributions and caused changes to the tax code through the years but the basic premise is still the same.

Why it came about: At the time, many businesses had pension plans for their employees, but not all did. So, this act created a way for people to save money in their own retirement accounts.

Pros:

- Available for all people with earned income, including non-working spouses of people with earned income (called a spousal IRA)

- Individuals can contribute up to $5,500/year (under age 50), and up to$6,500 (for those over age 50)

- May get a tax deduction for the amount of the contribution

Jill-splain this: If you make under the threshold of income (changes each year but in 2018, you had to make under $120k Modified Adjusted Gross Income (MAGI) if you were single or under $189K MAGI married filing jointly), you may be able to deduct your full IRA contribution on your tax return. - IRA contributions are protected in bankruptcy, up to $1,000,000

- Can name your own beneficiary, avoiding probate court

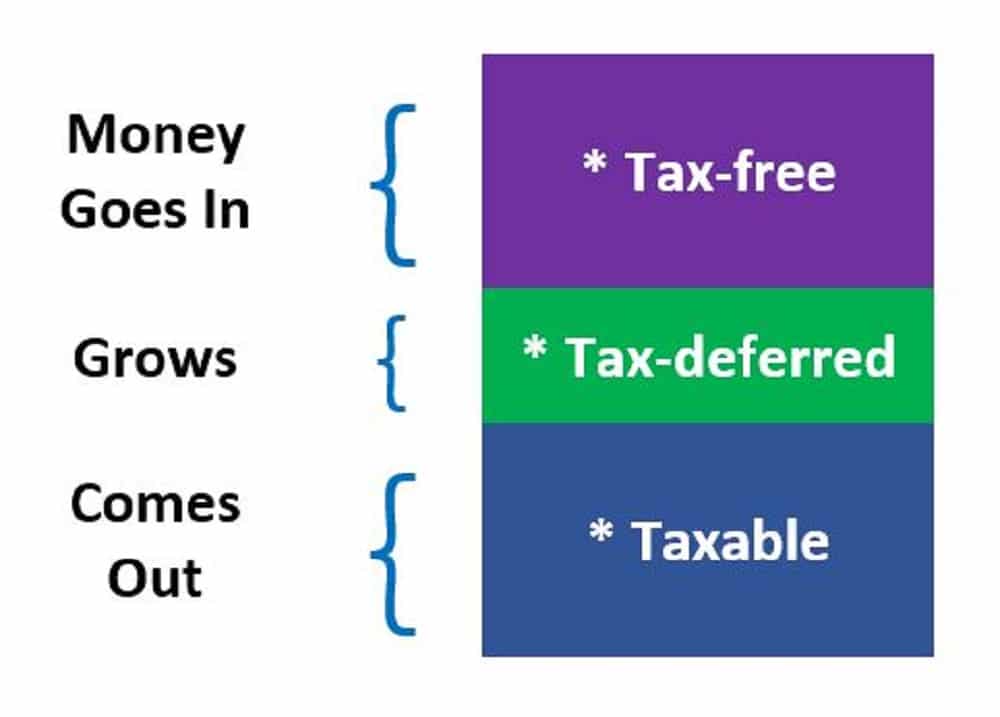

- Contributions grow tax-deferred—meaning, that if you earn dividends/interest/have growth on your investment—none of that is taxable to you until you go to take a distribution.

- Easy to open and you can open one almost anywhere (bank, investment firm, online, etc.)

- You control the investments, only limited by the options in place where you set up the account.

Cons:

- Not through employer, so no payroll deduction and you have to remember to make the contributions on your own

- Can’t contribute past the age of 70 ½ which is when you have to start taking mandatory distributions

- Can’t take money out until you reach the age of 59 ½ without a 10% penalty (with some exceptions)

- Distributions are taxable income to you (with some exceptions)

Income limitations on the deductibility of contributions (meaning, you are always able to put money into an IRA, but it may not be a tax-deductible contribution)

401(k) – named after the tax code section to which it applies, a 401(k) plan is an employer-sponsored retirement plan.

Quick History: A guy named Ted Benna, who worked for a small consulting firm, designed a plan for his own firm that was essentially the very first 401(k) in 1980. This type of plan caught on like hotcakes and now over 94% of private employers offer them.

Why it came about: Congress passed the Revenue Act of 1978 in order to try to limit high-earning executives from stashing their salary away in cash-deferred plans, thereby avoiding tax.

Pros:

- Higher contribution limits vs IRA: current limit if you are under 50 is $18,500, or $24,500 if you are age 50 and over

- Contributions are made pre-tax

Jill-splain this: Let’s say I make a $30k/year salary. I want to contribute 5% to my 401(k). This means I will contribute $1,500 to my 401(k) over the year. When I get my W-2, instead of box 1 saying I made $30k, it will say, I made $28,500. So when I file my taxes, I will report $28,500 as wages, even though I really made $30k. This makes the $1,500 pre-tax, because I am not paying tax on that income. - Protected from bankruptcy, up to a limit

- Can name your own beneficiary (although there are stipulations that if you are married, your beneficiary has to be your spouse, unless they agree not to be, which, could be awkward).

- Contributions grow tax-deferred

- Contributions can be made effortlessly through payroll deduction and changed at any time = easy

- Some employers offer a matching contribution or profit-sharing contributions

- May be able to borrow (take a loan out) against your 401(k) if you are in an emergency situation (not recommended, however).

Cons:

- Only have access to a 401(k) account through your employer so if they don’t offer one, you’re out of luck. However, you can be self-employed and open a 401(k).

- May not have as many options for investing as you would with an IRA, and the options may not be what you want. For example, you may not be able to buy individual stocks in your 401(k).

- Your company may have a waiting period–where you have to wait to be eligible to enter the plan

- Eventually, you have to start taking required minimum distributions.

- Can’t take money out until you reach the age of 59 ½ without a 10% penalty, if the plan allows this (with some exceptions).

Distributions are taxable income to you (with some exceptions)

It is important to note, that you can have BOTH a 401(k) and an IRA. A 401(k) is from an employer, whereas you can have an IRA on your own. So, both of these options are PRE-TAX, and sometimes referred to as “traditional” IRAs or 401(k)s. I’ll discuss the ROTH tax-deferred option of each of these in next week’s blog.

Disclosures

*Please remember that past performance may not be indicative of future results. Different types of investments involve varying degrees of risk, and there can be no assurance that the future performance of any specific investment, investment strategy, or product (including the investments and/or investment strategies recommended or undertaken by Stephens Consulting, LLC, doing business as Stephens Wealth Management Group (SWMG), or any non-investment related content, made reference to directly or indirectly in this newsletter will be profitable, equal any corresponding indicated historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. Moreover, you should not assume that any discussion or information contained in this newsletter serves as the receipt of, or as a substitute for, personalized investment advice from Stephens Consulting. Please remember that if you are a SWMG client, it remains your responsibility to advise us, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. To the extent that a reader has any questions regarding the applicability of any specific issue discussed above to their individual situation, they are encouraged to consult with the professional advisor of his/her choosing. SWMG is neither a law firm nor a certified public accounting firm and no portion of the newsletter content should be construed as legal or accounting advice. A copy of SWMG’s current written disclosure Brochure discussing our advisory services and fees is available for review upon request. Links are being provided for information purposes only. SWMG is not affiliated with and does not endorse, authorize, or sponsor any of the listed websites or their respective sponsors. SWMG is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members. Important Disclosure.

Please Note: Stephens Wealth Management Group does not make any representations or warranties as to the accuracy, timeliness, suitability, completeness, or relevance of any information prepared by any unaffiliated third party, whether linked to SWMG’s website or newsletter or incorporated herein and takes no responsibility for any such content. All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly.